The Rezoning Paradox

Why does every single person around me say housing sucks?

A finished housing development project across the street from a stripped down single family home about to be torn down and developed. This area (5 minutes from my house) was rezoned a year ago, allowing duplexes and townhouses to be built in place of single family homes.

The first question on the mind of almost everyone I know under 40 who isn't living with their parents: What's going on with housing? And from a policy lens, what can we actually do about it?

The answer many city councils have landed on is the YIMBY theory: remove restrictions, remove density limits, let the market build. The theory is genuinely sound and has worked in many places. Calgary implemented citywide blanket rezoning in August 2024, removing density restrictions across all residential neighborhoods. I wanted to see if it worked. Downtown Calgary construction, the Calgary Tower visible behind active development sites.

Downtown Calgary construction, the Calgary Tower visible behind active development sites.

The short answer: construction starts fell 16% below the pre-existing growth trend. The opposite of what was supposed to happen. More apartments, fewer single-family homes, but the total went down.

This doesn't mean YIMBY theory is wrong. It means something happens when a city council makes a wholesale decision on a market that was already moving. Imagine building a road with current traffic, eventually you increase capacity, but first you cause a traffic jam.

What I Wanted to Know

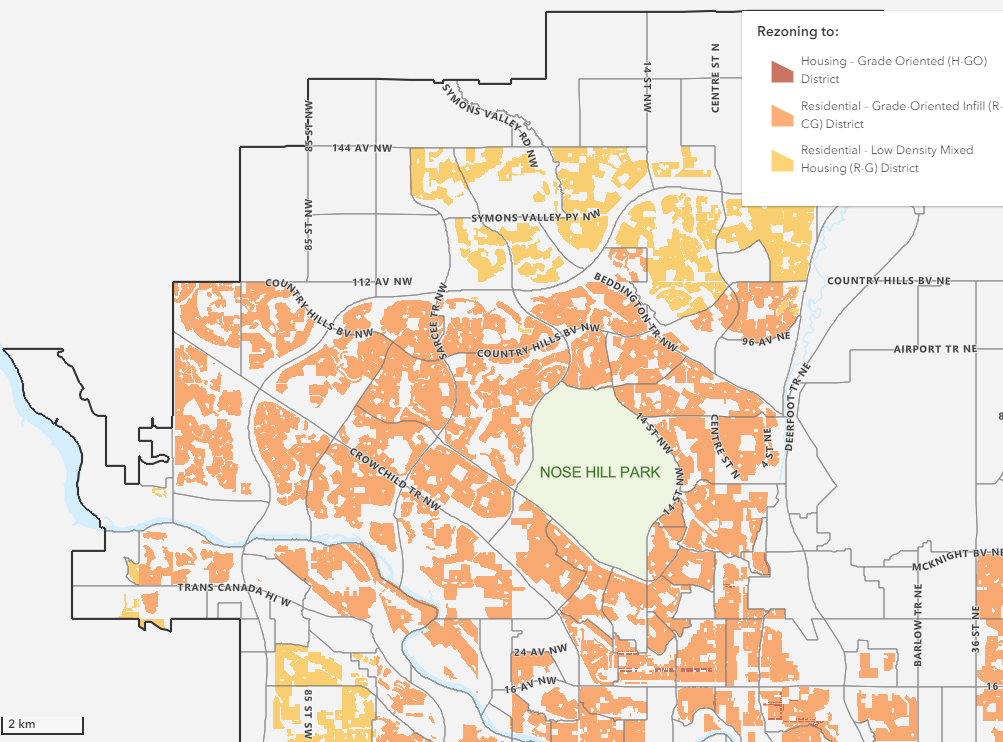

Did rezoning actually increase construction? Did it shift what kind of housing got built? And if the results didn't match the predictions, why? The City of Calgary Blanket Rezoning Map of Calgary's Northwest

The City of Calgary Blanket Rezoning Map of Calgary's Northwest

I used interrupted time series analysis, basically, comparing what actually happened to what would have happened if the pre-rezoning trend had continued. This lets you test whether the policy caused a change, or whether you're just seeing noise.

The Data

I used CMHC construction starts data, 17 months, November 2023 through March 2025. Construction starts capture when developers actually break ground, not when they file paperwork. It's the most direct measure of whether the market responded to the policy change.

| Data Category | Sources |

|---|---|

| Policy Changes |

Land Use Bylaw From City of Calgary Calgary's Housing Strategy 2024-2030 |

| Construction Data | CMHC Housing Starts and Construction Data |

I wanted to compare Calgary to Edmonton to control for provincial factors, but Edmonton implemented the same rezoning simultaneously. No control group. I wanted housing price data, but MLS databases cost $500/month and require professional credentials.The lowest pricing found was $500 per month for API access to already-sold houses. Live listings require a real estate license. I wanted community sentiment surveys, but the timing didn't align with the intervention date.

So: construction starts. That's what I could measure, and it's the leading indicator anyway, supply changes have to happen before price effects can follow.

What Changed?

| Year/Month | Single | Semi-Det. | Row | Apartment | Total |

|---|---|---|---|---|---|

| 2023-11 | 594 | 110 | 277 | 827 | 1,808 |

| 2023-12 | 538 | 160 | 282 | 513 | 1,493 |

| 2024-01 | 487 | 112 | 249 | 1,103 | 1,951 |

| 2024-02 | 460 | 154 | 279 | 781 | 1,674 |

| 2024-03 | 532 | 200 | 182 | 846 | 1,760 |

| 2024-04 | 528 | 198 | 228 | 877 | 1,831 |

| 2024-05 | 617 | 206 | 236 | 937 | 1,996 |

| 2024-06 | 719 | 210 | 307 | 730 | 1,966 |

| 2024-07 | 625 | 240 | 280 | 1,326 | 2,471 |

| 2024-08 | 597 | 198 | 328 | 552 | 1,675 |

| 2024-09 | 660 | 162 | 271 | 997 | 2,090 |

| 2024-10 | 644 | 220 | 454 | 1,372 | 2,690 |

| 2024-11 | 717 | 198 | 338 | 1,295 | 2,548 |

| 2024-12 | 514 | 154 | 360 | 689 | 1,717 |

| 2025-01 | 552 | 176 | 370 | 531 | 1,629 |

| 2025-02 | 500 | 238 | 279 | 1,390 | 2,407 |

| 2025-03 | 455 | 154 | 274 | 1,352 | 2,235 |

Initial analysis suggested a simple linear analysis at August 2024 shows a clear positive trend post-rezoning, indicating more housing and greater density. This tells a compelling story: remove restrictions on housing → more housing of different types AND more total construction.

However, a linear trend line at the intervention date wasn't sufficiently convincing. An Interrupted Time Series analysis was used to determine if this change affected housing beyond pre-existing trends. If rezoning was the treatment, what effect did it have on an immediate basis beyond the initial trend, and what behaviors did it elicit regarding post-rezoning trends?

The hypothesis was that housing would increase and become more dense, intrinsic to deregulating a particularly locked-in and heavily regulated market. The conviction remained that the trend wasn't as strong as implied by simple linear analysis.

The Real Analysis

I propose in this inquiry to take nothing for granted, but to bring even accepted theories to the test of first principles, and should they not stand the test, freshly to interrogate facts in the endeavor to discover their law. I propose to beg no question, to shrink from no conclusion, but to follow truth wherever it may lead.

The findings were paradoxical to the YIMBY deregulation theory of housing management. From November 2023 to July 2024, the actual growth rate was 72.0 construction starts per month. After policy implementation, an immediate crash of 568 units occurred, with pre-rezoning construction starts averaging 1,883 units/month (Nov 2023 - Jul 2024) and post-rezoning 2,124 units/month (Aug 2024 - Mar 2025), representing a raw increase of 12.8%.

However, the pre-policy growth trend was 72.0 units/month, and housing growth was increasing. Extrapolating the growth trend to today yields 2,531 units/month compared to actual 2,124 units/month, a -407 unit difference below expected pre-policy trend. Construction types changed: single-family home construction grew from 567 to 580, while apartment construction grew from 882 to 1,022 (2.3% and 15.9% respectively). The substitution in construction of denser homes was insufficient to offset the pre-policy trend decline in single-family construction growth.

The rezoning paradox is real. Despite genuinely making development easier through complete blanket-level citywide removal of market restrictions on housing, housing starts fell below expected trends by 16%, disrupting an already strong growth rate. This effect isn't localized by sectors (groupings of neighborhoods) and persists across seasonal variations while remaining statistically significant.

Figure 1. Interrupted Time Series Analysis

Hover over data points for exact values and differences from counterfactual projection. Click any point to lock tooltip and view detailed statistics. The intervention line marks August 2024 rezoning implementation. The dashed line represents projected housing starts had the policy not been enacted.

Y = β₀ + β₁(time) + β₂(policy) + β₃(time_after_policy) + ε

Where: β₀ = 1,524 (baseline) | β₁ = 72.0 (pre-policy trend) | β₂ = -568 (immediate crash) | β₃ = -54.2 (trend change after policy)

Figure 2. Housing Composition by Type

Single-family construction increased modestly at +2.3% while multi-family increased significantly at +15.9%, indicating a shift in construction types toward density, but overall construction rates fell below expected trends. Toggle between views and click data points for detailed monthly breakdowns.

Figure 3. Density Revolution: Multi-Family Ratio Over Time

The ratio of multi-family to single-family housing starts. Values above 2.0 indicate multi-family construction exceeds double that of single-family. Pre-intervention average: 2.32; post-intervention: 2.66, representing a 14.7% increase in density preference.

Statistical Robustness

Did uncertainty increase? Volatility before was 271, volatility after was 415 with an F-statistic of 2.34 (critical value: 3.29). The volatility increased but not significantly. Cohen's d = -1.18 indicates a large negative effect. Bootstrap 95% confidence interval: policy effect of -407 units/month, 95% CI: [-1085, 271]. The effect is statistically robust.

Calculation: d = (M_actual - M_expected) / SD_pooled = (2,124 - 2,531) / 345 = -1.18

Figure 4. Housing Type Trends at a Glance

Sparklines show 17 months of data in miniature. Each line reveals the pattern of construction starts over time.

| Housing Type | Trend | Pre-Avg | Expected | Actual | vs. Expected | % vs. Expected |

|---|

Gray vertical line marks the intervention (August 2024). Expected shows what would have happened if the pre-trend continued. Actual is the post-rezoning average. The comparison reveals the policy's true impact.

What Went Wrong (And How I Fixed It)

This project was initially conceived as comparative analysis. The intention was to compare Calgary post-rezoning to Edmonton, controlling for provincial and federal policy confounds by examining two cities within the same regulatory environment. However, Edmonton implemented similar blanket rezoning simultaneously, eliminating the natural control group. The initial research design was invalidated before data collection began.

The first set of research questions was too ambitious. I had proposed examining housing prices, rental rates, community sentiment surveys, crime statistics, and cross-city comparisons a holistic assessment of rezoning's effects across economic, social, and safety dimensions. This proved infeasible for three reasons. First, price effects lag construction changes by years; isolating rezoning's impact from concurrent federal mortgage reforms would require sophisticated controls unavailable with current data. Second, community sentiment surveys weren't available on timelines compatible with before-after analysis; Calgary's annual surveys don't align with the intervention date. Third, neighborhood-level crime and disorder data either weren't publicly distributed or lacked sufficient granularity for meaningful analysis.

Confronting these limitations forced methodological discipline. The project narrowed to a single empirical question answerable with available data: Did blanket rezoning increase construction starts? This question has the virtue of being both measurable and theoretically prior supply changes must precede price effects, making construction starts the leading indicator of policy impact.

The second major correction involved analytical approach. Linear regression suggested a clean story: upward trend post-intervention, consistent with YIMBY predictions, clean and simple. But this felt too convenient given the data's complexity and the intervention's scope. Simple before-after comparison ignores pre-existing momentum the Calgary construction market wasn't static before rezoning but already experiencing strong growth (72.0 units/month increase!). Any analysis failing to account for this baseline trajectory would misattribute natural growth to policy intervention.

Interrupted time series regression proved essential. It provides three parameters: baseline level, immediate jump at intervention, and trend change post-intervention. This structure captures what matters not whether construction increased in absolute terms (it did), but whether it increased beyond what would have occurred absent intervention (it didn't). The counterfactual projection what trend-line extension predicts for post-intervention months became the comparison point. Actual construction ran 407 units below this projection, a 16% shortfall.

The lesson extends beyond this project. When testing policy interventions, resist the temptation to find confirming evidence in absolute changes. Markets have momentum. Economies have trends. The question isn't "did things change after the policy" but "did they change differently than they would have anyway." This requires modeling the counterfactual explicitly mnot as speculation but as quantitative projection from pre-intervention data. When actual outcomes diverge from well-founded projections, that gap measures policy effect. In this case, the gap was negative and large.

Methodological humility also means acknowledging temporal constraints. Less than one year post-intervention provides insufficient data for definitive conclusions about long-term effects. Construction markets operate on multi-year cycles. from concept to occupancy takes 18-36 months depending on project scale. We observe immediate disruption clearly. This analysis documents what happened in the short term and identifies mechanisms likely responsible. Whether these mechanisms resolve or persist requires patience and continued observation.

The Cost of Victory

These photos are all within five minutes of my house. Empty lots, torn-down single-family homes not yet developed. Families who took the money and moved, leaving literal holes in the community. Those holes are hopefully filled with new tennants, new families moving into denser communities creating spaces of shared value, but the abrupt scale of changes and market volitality has caused lots to be bought and to be held without new neighbours.

There's a handmade birdhouse, maybe made as a summer project by a parent and child, left hanging in the ruins of their house. You can see where the house was ripped open and where the birds were meant to nest when returning from winter.

Lower rent prices, more dense buildings, more construction these are good things worth striving for. But when changes are made, and those promises aren't delivered, the people who made up a thriving community took the real estate value and cashed out. With no fault to them, it leaves a feeling of emptiness. It leaves literal holes.

Why Did This Happen?

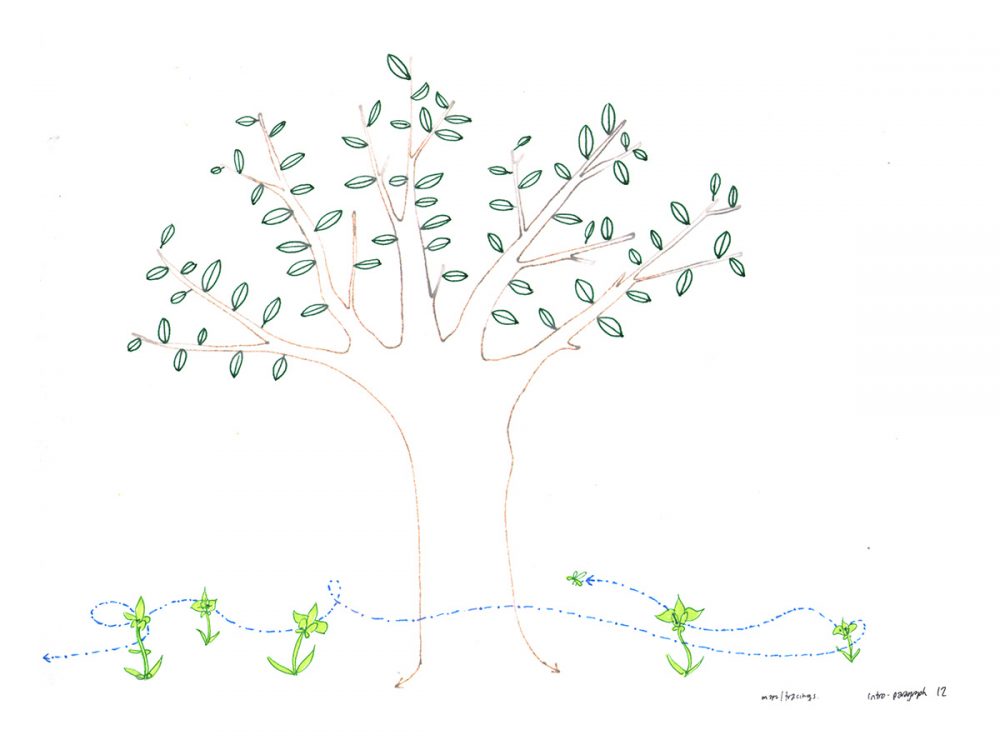

Tree logic: one trunk, branches splitting downward. The rhizome runs beneath, connecting without hierarchy.

Tree logic: one trunk, branches splitting downward. The rhizome runs beneath, connecting without hierarchy.

Magda Wojtyra & Marc Ngui, Drawing a Thousand Plateaus

City councils work like trees. One trunk, branches splitting downward. Thirteen people vote yes or no, and it applies instantly to 260,000 lots. That's how hierarchies work, one decision ramifies down through everything beneath it.

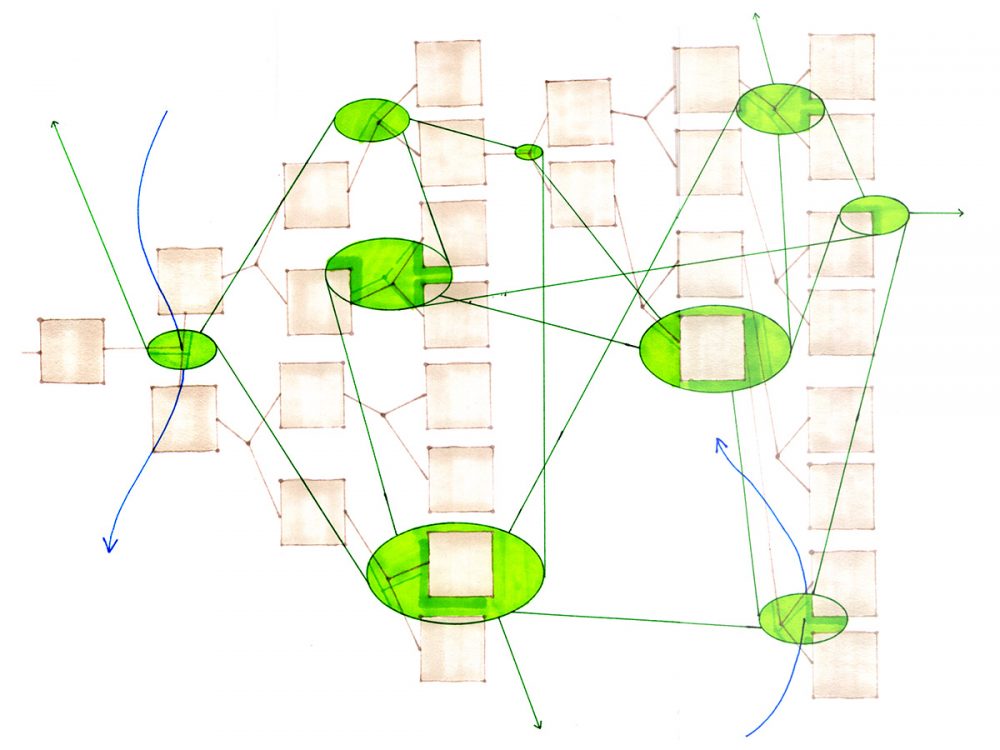

The grid is the city's zoning map, fixed, hierarchical. The green nodes are the relationships that actually make things happen: contractors who know each other, developers who've worked with certain banks, knowledge that spreads through coffee conversations. The network grows on top of the structure, not because of it.

The grid is the city's zoning map, fixed, hierarchical. The green nodes are the relationships that actually make things happen: contractors who know each other, developers who've worked with certain banks, knowledge that spreads through coffee conversations. The network grows on top of the structure, not because of it.

Magda Wojtyra & Marc Ngui, Drawing a Thousand Plateaus

Construction markets work like root systems. No center. A developer needs financing from a bank that's willing, permits from a department that's staffed, contractors who know the technique, suppliers with materials in stock, buyers who want to live there. Each connection is separate. Each has its own logic. A project only exists when all of these align at once.

The council changed one thread: zoning. But banks still had loan products for single-family homes. Contractors still had crews trained for single-family builds. The relationships that made projects work under the old rules didn't automatically translate to the new ones.

That's the paradox. Construction fell not because rezoning was wrong, but because you can't command a network to reconfigure. Banks don't update their risk models because a bylaw passed. Contractors don't learn new techniques overnight. Developers don't know which lenders will fund townhouses until they ask around. These connections form slowly, through experimentation and word of mouth. Some developers figure it out; others learn from them; knowledge spreads.

The 16% gap between what we got and what the trend predicted is the cost of treating a root system like a tree.

The Collision: Arborescent (city council) logic VS Rhizomatic (contractors and developers)

What This Means for Policy

The lesson isn't that rezoning was wrong. Calgary's zoning code was genuinely restrictive. The lesson is that big instant changes to networked systems cause disruption proportional to their speed and scope.

An alternative: phase it over three years across different neighborhoods. Early areas become laboratories, developers experiment, lenders develop products, contractors learn, knowledge spreads. Later areas benefit from what's already been figured out. Slower, but the momentum never breaks.

Or keep the blanket approach but provide transition support. Bridge financing for developers mid-project. Fast-track permits for first-movers. Training programs for contractors. Not subsidies, infrastructure investments acknowledging that the city's decision imposed real costs on people who now have to rebuild their networks from scratch.

The deeper point: most systems we try to govern aren't trees. Markets, ecosystems, communities, they're webs. They don't respond to commands like machines. They adapt through distributed experimentation, and that takes time. If we want big transitions, we have to design for that.

The same lot, late August. The house is gone now. Although change is slow and painful, I remain hopeful that something is being built for the better, not just in my neighbourhood, but across the city.